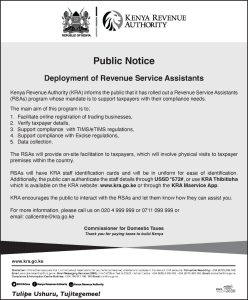

Revenue Service Assistants (RSAs) are newly hired field officers employed by the Kenya Revenue Authority (KRA) and are part of the Domestic Taxes Department. They are stationed and active in various Tax Service Offices (TSOs) throughout the country.

The primary responsibility of RSAs is to conduct on-site visits aimed at overseeing compliance and supporting efforts to broaden the tax base. These actions align with KRA’s overarching mission of collecting revenue on behalf of the government.

In a recent encounter that has generated quite a buzz, Antony Walela, a seasoned businessman with decades of experience, shared his interaction with newly deployed Kenya Revenue Authority (KRA) Revenue Service Assistants (RSAs) on social media. The encounter raised questions about the extent of their authority and the need for clear boundaries when engaging with businesses.

Taking to Facebook, Antony Walela described the unexpected visit by a group of six young men and women, all donning KRA uniforms. He began his post by stating, “Today, 6 young men and women walked into my shop. They were all in KRA uniform.”

Mr. Walela’s extensive business experience had previously exposed him to various regulatory bodies, including the police, regulatory officers in the pharmacy sector, and local authorities, but never before had he encountered KRA officials in such a manner he says.

The RSAs, as part of their duties, asked Mr. Walela a series of questions related to KRA compliance and requested various business documents. In his commitment to being a law-abiding citizen, he readily provided the necessary documents, including county government licenses.

However, he began to question the scope of their authority when the RSAs ventured beyond KRA-related matters.

“They even went beyond KRA issues and requested to have a look at County Government licenses (IS THIS COLLABORATION?),” Mr. Walela asks.

After being nice to them, Mr. Walela found himself compelled to set boundaries after he felt that the RSAs were overstepping.

He says, “However, I had to turn around and become difficult when I realized my good manners were being misused.” When confronted with questions about his business turnover, property ownership, and rent payments, he insisted that such details should be obtained through official channels and annual returns, rather than in an informal visit.

{kind=link}